Forty years ago, Harvard political economist Paul Peterson identified the fundamental constraint cities face: they cannot effectively tax mobile factors — residents and businesses will vote with their feet and leave, eroding the very base being taxed.

Philadelphia’s population history is Peterson’s theorem made real. The city peaked at 2.07 million residents in 1950. It has lost population in nearly every decade since. It sits at approximately 1.6 million today — roughly flat since 2010 — while the four surrounding Pennsylvania counties have grown 5 to 12 percent in the same period.

This is not a coincidence. It is what happens when a city spends 70 years taxing the most mobile factor it has — the people who choose where to live — at the highest rate in the region. The wage tax is not incidental to Philadelphia’s population decline. It is a structural cause of it. And Philadelphia’s fiscal trajectory follows directly from that decline: a shrinking base, rising rates to compensate, more residents leaving, a smaller base still. That is the cycle. The population data is the proof.

The 2025 Tax Reform Commission recognized the problem. But incremental reform cannot solve a structural problem. Philadelphia has been “reducing” the wage tax since 1996. Thirty years later it is still 3.75 percent. The reform enacted this year conditions its most meaningful changes on pension fund milestones that may not be reached until 2040. This is not a plan. It is a press release. The city cannot afford to wait another 30 years for another rounding error.

This proposal does something different. It does not tinker at the margins. It restructures the entire tax system around Peterson’s insight: Stop taxing the things that can leave, and tax the one thing that cannot — the act of selling into a market of 1.6 million consumers.

I attempted a portion of this when I was a City Councilmember from 2008 to 2014. My proposal at the time was simpler, just involving business taxes. This is progressive compared to the current system by a lot. It would also create lots of jobs over time.

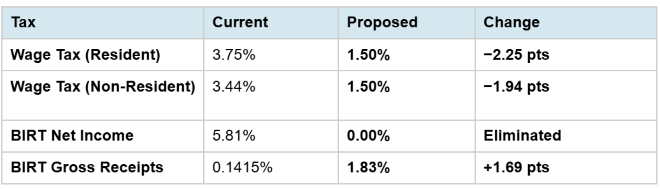

What Changes: Three Numbers

No new taxes. No new bureaucracy. No enabling legislation required. The gross receipts tax already exists. Wage tax withholding already exists. This changes three rates. Workers see more money in their next paycheck. Businesses report quarterly sales instead of estimating annual profits. It is simpler than what we have now.

What This Means on Day One for Philadelphia Businesses

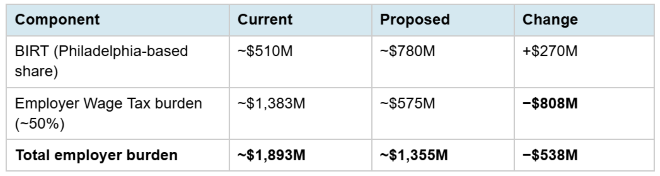

The current system penalizes businesses for being here. Two-thirds of BIRT net income revenue comes from Philadelphia-headquartered companies. Eliminating net income and expanding gross receipts reverses that — two-thirds of the expanded gross receipts base is paid by businesses headquartered outside Philadelphia that sell into this market.

Philadelphia-headquartered businesses save $538 million in combined tax burden. BIRT rises $270 million, but the reduction in wage tax incidence saves $808 million. The entire increase in business taxation — and far more — is paid by businesses headquartered outside Philadelphia that sell into this market. Every national retailer, every out-of-state service provider, every e-commerce company delivering to Philadelphia addresses pays for the privilege of accessing 1.6 million consumers. The owners of Philadelphia’s businesses — the partnerships, LLCs, and sole proprietors who pay the Net Profits Tax — also see their personal rate fall from 3.75 percent to 1.50 percent, matching the wage tax reduction.

For Philadelphia Residents

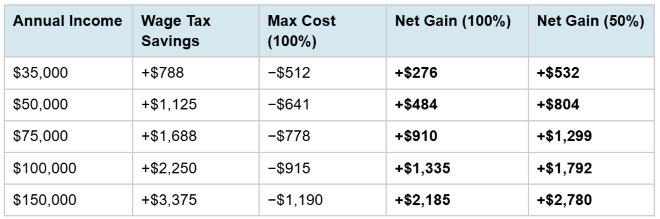

Workers come out ahead at every income level, even assuming businesses pass 100 percent of the gross receipts increase to consumers.

For a worker to lose money even in the worst case, their Philadelphia spending would need to exceed 123 percent of their gross income. That is mathematically impossible. Workers come out ahead at every income level, under every scenario.

Pennsylvania caps municipal earned income taxes at 1 percent for most municipalities. At 1.50 percent, Philadelphia is within 50 basis points of what most surrounding suburbs charge — the smallest gap in modern history. The penalty for living in Philadelphia nearly disappears. For the first time in decades, the wage tax stops being a reason to leave.

What This Means Over Time: The Flywheel

Revenue neutral on day one is not the full story. It is the floor.

$1.6 billion returns to Philadelphia wage earners annually. At a 65 to 70 percent local spending rate, approximately $1.0 to $1.1 billion flows directly into the Philadelphia businesses where those earners live and shop. Those businesses hire more. More hiring means more income. More income means more spending. More spending means a larger gross receipts base — generating more revenue without raising rates.

Meanwhile, the lower wage tax changes the residential calculus. The young professional who would have moved to Conshohocken stays in Fishtown. The dual-income household that would have bought in Ardmore buys in Chestnut Hill. The remote worker who can live anywhere finds the math no longer punishes them for choosing Philadelphia. More residents means more property tax revenue. More property tax revenue means better-funded schools, cleaner streets, more police, and services for the most vulnerable — the quality-of-life investments that make a city a place people actively choose. Which attracts more residents. Which generates more revenue. The flywheel runs forward instead of in reverse.

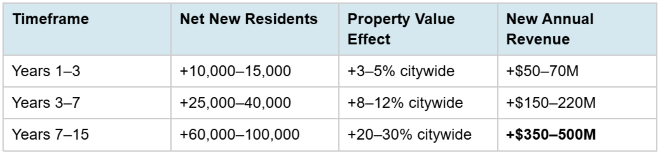

The numbers are not speculative:

At the high end — 100,000 net new residents over 15 years — Philadelphia would be back to its 2000 population trajectory and generating $400 to $500 million in new annual revenue without raising a single rate. That revenue funds better schools, cleaner streets, safer neighborhoods, and homeless services that make the city livable for everyone. Those improvements attract more residents. Which generates more revenue. Which funds more improvements.

The current tax structure cannot produce this outcome. It can only produce more of the same — a city that exports residents, shrinks its base, and oscillates between raising taxes and cutting services on an accelerating timeline. Philadelphia’s population has been roughly flat for fifteen years. The four surrounding counties have grown. That is not homeostasis. That is decline at a sustainable pace — until it isn’t.

The Urgency

This proposal requires acting now for a simple reason: restructuring requires reserves to absorb the transition period while new revenue patterns stabilize. Philadelphia currently holds approximately $1.1 billion in reserves — built on one-time federal relief funds that are now fully obligated. The Controller projects those reserves will fall to $45 million by FY2029. After that, only two choices remain: raise taxes that accelerate decline, or cut services that make the city less livable.

In 2010, Mark Zandi, chief economist at Moody’s Analytics, told Philadelphia City Council that this restructuring was “sounder from an economic theory perspective” than the city’s existing structure — and that it would produce results with “perhaps an even greater effect given the smaller boundaries of the taxing jurisdiction.” The legislation passed committee 6–2 in 2013 and never became law.

Peterson’s mobility constraint has run Philadelphia’s flywheel in reverse for 70 years. The population data is the proof of what happens when you do nothing. The revenue table above is the proof of what happens when you act. The window is open now — while reserves exist, while the framework is understood, while the political will can be marshaled. It will not stay open.

Set the rates. Set a date. End the debate.

Bill Green is a former Philadelphia City Councilmember At-Large and former chair of the School Reform Commission.

The Citizen welcomes guest commentary from community members who represent that it is their own work and their own opinion based on true facts that they know firsthand.

![]() MORE ON PHILLY TAXES

MORE ON PHILLY TAXES