Earlier this week, Arizona Senator Ruben Gallego released his housing plan to rebuild the American Dream and restore affordability. It’s good and worth a read. Great to see a potential 2028 candidate producing a report like this.

Lauded by YIMBY and Abundance leaders, the plan’s primary perspective is that we need to build more housing to solve the affordability problem. Gallego is a savvy politician who understands that men want to own a “big ass truck” and move out of their parents’ home. He knows the American dream of homeownership is a winner.

But, to bastardize Langston Hughes, what happens to an American dream deferred? As Gallego’s proposal notes, the median age of a first-time homebuyer has been steadily increasing. It’s now 40, when in the 1980s it was about a decade younger. The reasons why Americans are buying their first home so much later has to do with a lot of factors, but obviously the high cost of housing is one of them.

Gallego’s report notes:

First-time homebuyers increasingly cite the inability to afford a down payment as the primary barrier to purchasing a home. A buyer needs $26,800 for a 3.5 percent down payment on a median priced home — an amount only 12 percent of renters possess. For a 20 percent down payment, they would need $95,000, which only 4 percent of renters have saved.Millions of millennials — now 40 or younger — have the credit characteristics to qualify for a mortgage but lack the savings for a down payment, suggesting this really is one of the major barriers standing between them and homeownership.

But despite noting that saving for a down payment is a primary obstacle to buying a home, of the report’s 54 policy recommendations, just two offer solutions on this issue: reducing the amount required for down payments, and even eliminating it for first responders, teachers and the like.

There’s also a bit of cognitive dissonance: Building more housing doesn’t solve the problem of saving for a down payment. Programs that help renters build assets do.

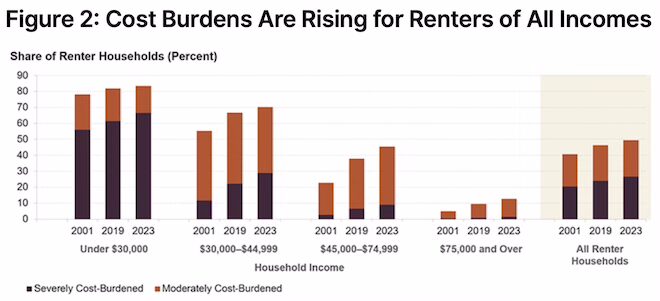

About half of renters are moderately or severely cost-burdened these days. In those cases, they may be barely able to afford essentials, with no room for savings.

At the same time, the problem is not just that renters are excluded from the American dream, but excluded from it for a longer period of time. People are missing out on the economic advantages of homeownership for a greater portion of their prime earning years as they delay homeownership. There are two ways to solve that problem — one is to try to make everyone homeowners sooner (the hope of many, many housing plans). The other, which is less discussed, is to make renting an asset building strategy so that people don’t lose out on asset building entirely for the decades before they are homeowners.

It’s an amazing day to see such a thorough proposal like Gallego’s and feel like it’s a bit “table stakes” at this point. I’d love to see more politicians recognize that we don’t just need to lower the cost of homeownership and rent, but that renters need a bit of the American dream, too. They need more vehicles to save money and to build equity.

A renter plan that acts like a 401(k) or 529

We are nearing the 50th anniversary of the modern 401(k) plan. We’ve embraced the idea of taking pre-tax dollars and saving them for retirement. We could create a similar vehicle to save for a down payment. We need a renter’s 401(k) — which employers themselves can match contributions to, rather than picking and choosing who is worthy of getting down payment assistance.

State treasurers could also devise a savings infrastructure similar to their statewide 529 plans, which enable people to invest in funds that grow modestly over time, then withdraw the funds without capital gains. Except instead of withdrawing for education, this plan would allow people to withdraw for the purpose of buying a home.

Tenant equity growth

We also need more methods for renters to get some of the upside of real estate. This month, Colorado launched its Tenant Equity Vehicle — a first in the country program that enables affordable housing tenants to receive “equity” payments for their rent. As Next City reported last year:

In 2022, Colorado voters approved Proposition 123, which set aside 0.1 percent of the state’s income tax revenue for affordable housing programs. This includes familiar programs like housing vouchers and down payment assistance for home purchases. But Proposition 123 also included a unique program that would allow tenants of new affordable housing financed by the initiative to be paid the “equity” for the homes they rent, in theory giving them some of the financial benefits a homeowner might get.

Colorado Governor Jared Polis announced the first five projects for the program last month. It’s a model that other states could replicate.

Cash back programs

Enterprise Community Partners has also created a renter wealth creation fund that enables donors and investors to invest in properties where renters get cash back for on-time payments and opportunities for shared appreciation when a property is sold.

There is tremendous interest in finding ways for renting and mortgages to generate more savings for people. The massive amount of buzz over changes to Bilt’s rewards program for renters and mortgage payers shows that there’s a desperate hunger to get some financial rewards from housing outlays.

Unfortunately after all the hype on Bilt, the result seems to be just that they’re capping their interest rates at 10 percent to be in line with any future federal regulation.

Building more housing and providing more housing options is a necessary part of any plan to attack affordability. But it doesn’t address the fact that people are missing out on a critical life-defining period of asset building as renters. The real American dream would be one that is accessible to all Americans — not just homeowners.

Diana Lind is a writer and urban policy specialist. This article was also published as part of her Substack newsletter, The New Urban Order. Sign up for the newsletter here.

![]() MORE FROM THE NEW URBAN ORDER

MORE FROM THE NEW URBAN ORDER